Valued at approximately $1.48 billion in 2025, Oberlin College’s endowment fuels many aspects of College operations from financial aid to faculty salaries. Yet its size is also the subject of ongoing conversation about how the College allocates its resources and whether that spending aligns with students’ lived experiences on campus.

Student organizations, including Students for a Free Palestine and Students for Energy Justice, have called for Oberlin’s Board of Trustees to divest the College’s endowment from ventures that they believe compromise the College’s moral integrity. Local labor advocates have similarly pointed to Oberlin’s endowment to argue that the College has a responsibility to hire unionized workers and pay them well — a particularly fervent point of contention when the College decided to outsource over one hundred janitorial and dining jobs in 2020.

The endowment is central to debates about Oberlin College’s financial priorities and future. This article aims to answer some of the most common questions surrounding it.

What is a college endowment, and how does it work?

A college endowment is a pooled fund of donated money that is invested to support the institution over time. At Oberlin, donations are either unrestricted, meaning the College can use them at their own discretion — often for its highest-priority needs — or restricted, meaning they must be used for a specific purpose defined by the donor. Oberlin reports that a large share of unrestricted giving supports financial aid, with about 87 percent of what the College pulls from the endowment is directed toward scholarships. By contrast, restricted gifts can fund targeted initiatives. For instance, donor-backed funding has supported the development of specific academic programs such as the business program funded by Alan Wurtzel, OC ’55, and Irene Wurtzel.

Oberlin’s endowment is made up of roughly 1,350 individual funds and is invested in a diversified portfolio. Like many peer institutions, Oberlin follows a version of the “Yale model,” an investment strategy characterized by allocating significant portions to alternative assets such as private equity, venture capital, and private credit alongside traditional holdings like public stocks and bonds. This strategy is designed to generate higher long-term returns and spread risk across different markets, though it can also make funds less liquid and returns more variable year to year.

How has our endowment grown over time?

Oberlin’s endowment has roughly tripled since 1999. This increase is shaped by market cycles, fundraising campaigns, investment strategy, and institutional spending decisions.

In the early 2000s, as the endowment climbed from roughly $525 million to $682 million, the College financed significant expansion with major construction projects, issuing bonds in 2003 ($40 million), 2005 ($50.1 million), and 2006 ($25.1 million).

This growth was interrupted by the 2008 financial crisis, when the endowment fell sharply to about $537 million in 2009. The early 2010s marked a period of recovery and restructuring: Oberlin adjusted its investment reporting methods, launched the Illuminate campaign (raising $317 million by 2016), and continued issuing bonds while also managing rising costs through measures like voluntary retirement incentives.

Through the late 2010s, the College combined strategic restructuring with continued borrowing. This included the One Oberlin Plan and refinancing efforts in 2019. During the pandemic era, despite operational disruptions, the endowment surged, reaching over $1.27 billion in 2021, largely as a result of strong financial markets and investment gains. However, this growth remained volatile, with returns swinging dramatically, with a 42 percent gain in 2021 followed by a 4.9 percent decline the next year. By 2025, the endowment reached approximately $1.48 billion.

Can the College take money out of the endowment?

Yes, but only in a limited and structured way.

Rather than spending these donations directly, colleges invest them and withdraw only a small percentage each year. There are constraints on this: many funds can only be used for specific purposes defined by donors, and additionally, spending too much too quickly would shrink the endowment over time, undermining its long-term role.

At Oberlin, this “payout rate” is typically around 4-5 percent annually and supports operations like scholarships, faculty salaries, and facilities. During crises, colleges sometimes increase payouts. For example, Oberlin’s payout rate rose to roughly 6.7–6.8 percent in the years following the 2008 financial crisis, showing heavier reliance on endowment funds when other revenues were under pressure. But this is generally temporary, since higher draw rates are not sustainable long-term.

Using the NACUBO-Commonfund Study of Endowments, Oberlin’s payout rate lines up closely with peer institutions of similar size. While the report doesn’t isolate a single exact bracket for ~$1 billion endowments, institutions in adjacent tiers (hundreds of millions to multi-billion) show similar behavior, generally noting a payout rate around 5 percent.

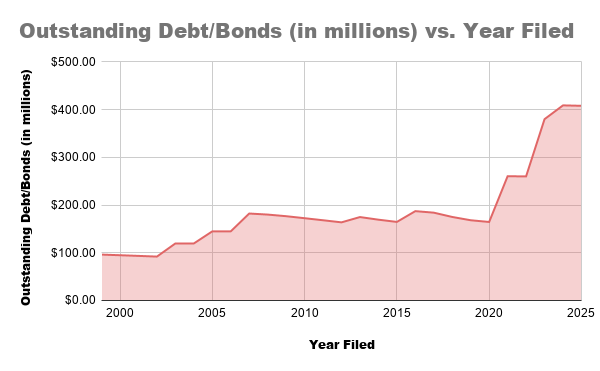

Does having a billion-dollar endowment mean that we don’t have debt?

No. Oberlin’s debt has risen significantly from about $260 million in 2022 to over $408 million by 2025, reflecting decades of bond issuance for projects (e.g., campus construction, refinancing, and green bonds).

Having a large endowment does not mean an institution is debt-free because debt is often used strategically to finance long-term capital projects. At Oberlin, this can look like projects such as the Sustainable Infrastructure Program, construction of new buildings, and infrastructural changes.

Moreover, the endowment is not fully liquid. Much of it is invested in long-term or illiquid (not easily convertible to cash) assets, and much of it is restricted, so it cannot be used to pay off general expenses or debt.

How does our endowment relate to endowments at other schools?

The national landscape of higher education is defined by stark disparities in endowment size and performance. Within Ohio, Oberlin’s endowment is the fourth largest in the state — $6 billion dollars short of the Ohio State University, which ranks number one. Oberlin’s endowment ranks 116th amongst the 500 largest in the nation. While institutions are facing a heightened risk of closure or merging with other institutions, Oberlin has remained safely above the water.

Over the past decade, Oberlin’s investments have yielded revenues that rank within the top 25 percent of similar institutions with endowments of a size between $1 billion — $5 billion. Still, the College’s endowment represents a fraction of the pool of endowed funds enjoyed by the nation’s top 10 institutions. Columbia University, which holds the 10th largest endowment, is $10 billion larger than Oberlin. Harvard University, which is ranked number one, has an endowment worth roughly $52 billion more than Oberlin.

How much information about the endowment is publicly available?

The College publicly discloses these figures through its annual 990 forms, which are mandatory for most nonprofit institutions to file. Though those figures are publicly available, the exact funds Oberlin has invested its endowment into over the years are generally private.

This article is part of a series that aims to examine Oberlin’s finances in greater depth. Should readers have questions they would like to bring to our attention, they can email newseditors@oberlinreview.org.